The S&P 500 had a fast start to the third quarter of 2021 only to be held back by September’s -4.7% return, marking the first monthly drop since January. Despite a poor September, the S&P 500 managed a 0.6% return for the third quarter. Market volatility picked up after being relatively contained since the beginning of the pandemic in early 2020.

While we remain positive about the global economy on a nine to 12-month horizon, equity markets struggled in September due to several short-term risk factors: Peak growth; prospects for a tapering later this year; negative policy and economic developments in China; and U.S. politics.

We would be much more concerned of these risks if global central banks decided that the inflation upturn was indeed durable (and not transitory), and they needed to curb economic activity sooner by raising rates before 2023 – which is what the market is currently pricing. As a reminder, in May 2013, Fed Chair Bernanke announced that the Fed would begin reducing the volume of its asset purchases but gave no clear timeline. The announcement caused considerable, albeit temporary, bond and equity markets turmoil, and was referenced as the “Taper Tantrum of 2013.” The Fed ended up delaying any action before gradually slowing its asset purchases until January 2014. We don’t want a Taper Tantrum repeat.

By now, the supply chain issues and their impact on the economy as well as the elevated measures of inflation are well documented and understood by the market. Get your Christmas shopping done early as we may run out of inventory!

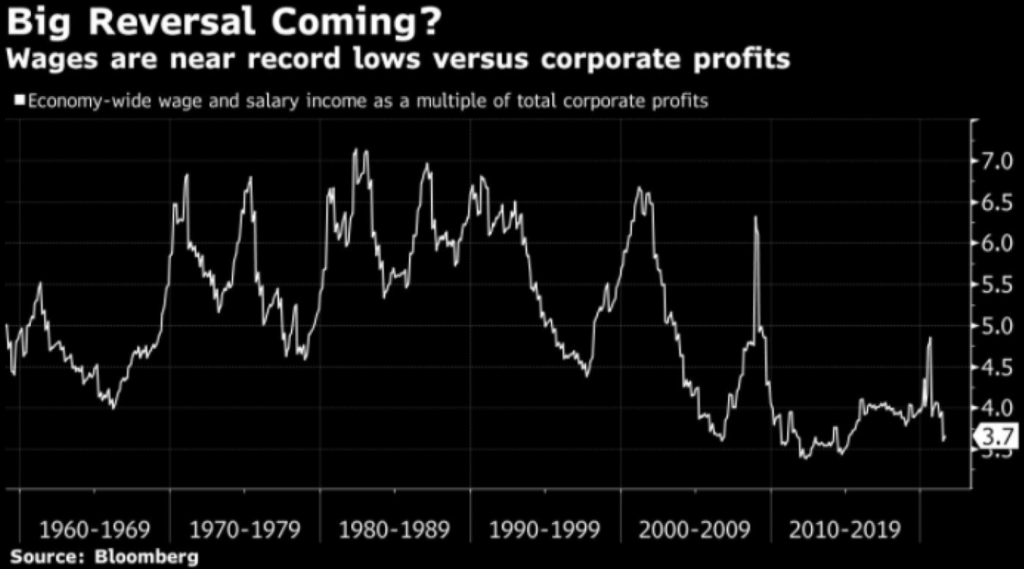

At our last Investment Committee meeting, the team debated the impact of wages as the potential game changer when it comes to making inflation more “sticky.”

What is happening in the labor force post COVID has surprised many. Old relationships have not held true so far, and the data reflects that.

The Harvard Business Review calls it the “Great Resignation.” According to the U.S. Department of Labor, a total of 11.5 million workers quit their jobs during the months of April, May, and June 2021. It’s not over. In July the U.S. hit an all-time high of 10.9 million job openings.

Higher wages have the potential to cut into corporate margins, and this upcoming third quarter earnings season will be a good test to that thesis.

Finally, as we bring it back to asset allocation, we remain steadfast in being underweight Fixed Income as well as having some exposure to TIPs to diversify portfolios away from (higher) interest rate risk.

If you have any questions or want to have a conversation about the market or your portfolio, please contact Liz, Ed, Fred, Scott, Tyler, or myself. Your Sendero team is ready to help.

Amaury de Barros Conti

Partner | Vice President Investments

210-930-9409

aconti@sendero.com